Cost saving is an unofficial goal for every business on the face of this planet.

Thriving in a competitive business landscape comes with a little bit of sacrifice. Most times, the sacrifice would be cutting costs.

But to reduce accounting costs, you have to think bigger than budgeting or expense control.

It requires you to invest in integrative technology that improves business efficiency and minimizes manual labor.

Let’s explore the critical areas you can work on to reduce accounting costs.

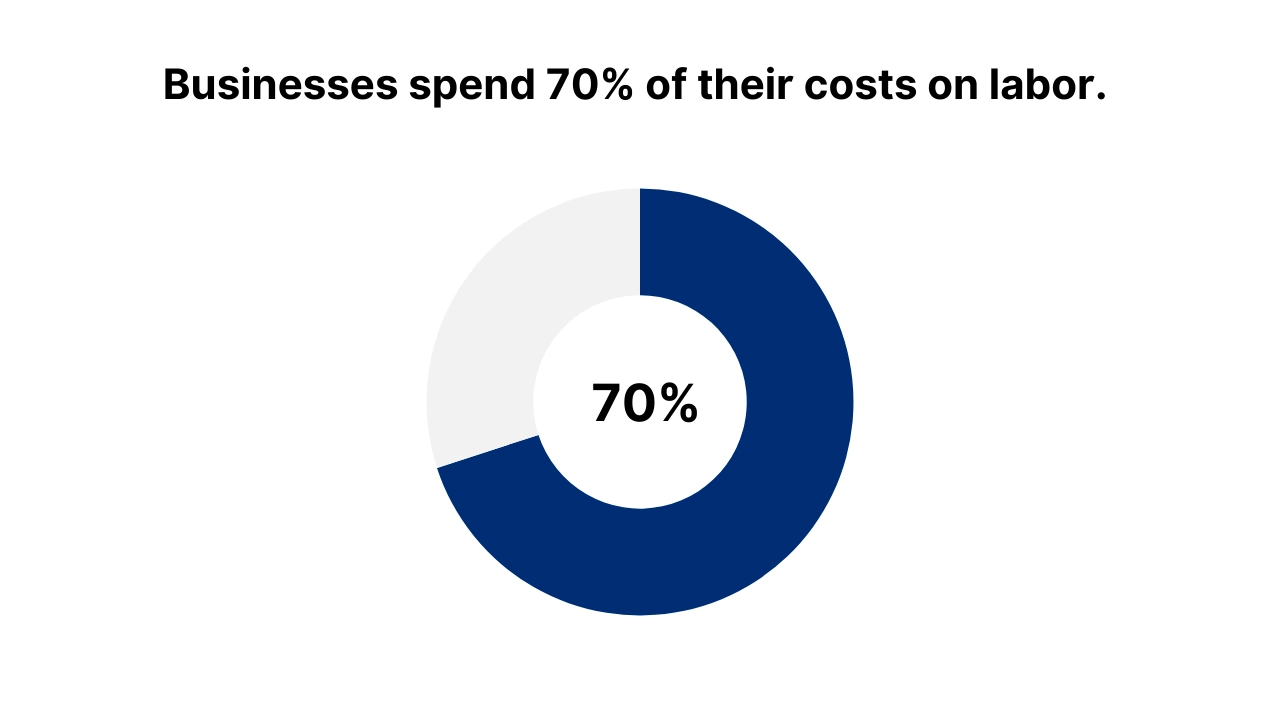

- Businesses spend 70% of their costs on labor.

- 25% to 35% of costs go into inventory management.

- 43% of cost reduction initiatives fail due to poor strategy and unrealistic goals.

Exploring cost reduction for businesses

Most businesses spend about 70% of their cost on labor, while 25% to 35% of the cost goes into inventory management.

Both of these aspects are crucial for running a business. You need your people and you need to manage your inventory.

So where and how does cost reduction come into play?

Well, let’s understand what cost reduction really is.

Cost reduction can be described as those unnecessary expenses on your company’s bottom line.

This may be the overhead that you paid some vendor or the cost of dead stock in your inventory that could’ve easily been avoided.

Sometimes it is the salary of the full-time employee you’ve hired whose work can easily be outsourced at a much lower cost.

Now, how can you reduce this cost entirely?

Well, first you must understand that every business is different and has a unique way of doing things. So, there’s no one glove fit all situation happening here.

Another thing that you should keep in mind is that this is an ongoing process. This means constant reflection and coming up with strategies to minimize costs.

7 ways to reduce accounting costs

43% of cost reduction initiatives fail due to poor strategy and unrealistic goals.

The only way you can succeed in reducing accounting costs in business is to implement and execute a clear strategy.

Here are 7 ways you can reduce your accounting costs.

1. Evaluate accounting costs

Businesses should conduct regular account evaluations to see where they are profiting and where they can improve.

But what exactly comes in accounting costs?

Well, it is any cost that you track in your financial records to reflect on your financial statements.

Thus, it is important to maintain accurate financial records as it helps with cost reduction.

Fixed and variable costs

When you evaluate your accounts, you also categorize your costs to make the information simpler and easier to understand.

So, you can categorize your costs into fixed and variable costs.

Fixed cost includes any expense that is the same throughout the year. An example would be the rent you pay or the salaries you credit into your employee’s bank accounts.

Variable costs, on the other hand, include any expense that changes according to the production level or is dependent on any external factor that is beyond your control, like sales and the cost of raw materials.

Cost per unit

The next aspect you should consider is the cost per unit.

The total cost of one unit of production is your cost per unit. We’re talking about the product or service you sell, of course.

You can calculate it by dividing the total cost of production by the total units produced.

You may wonder why this metric is important.

Well, it helps in cost analysis so you can identify business processes where you can save money and increase profitability.

In-depth understanding of accounting principles

If you run a business, you should explore and understand the depths of cost accounting principles.

- They help you identify and categorize your costs correctly.

- They give you perspective on how to allocate your money best.

- They help you analyze your spending behavior.

With this information, you can get a more accurate picture of your business’s financials.

You’ll be empowered to make informed decisions to support your cost-reduction efforts.

2. Improve workflow efficiency

When you work on improving your workflow efficiency, everything, like cost reduction, falls into place.

There are several benefits to workflow efficiency. For example:

- Increased productivity

- Reduced manual input

- Cost saving

- Time management

Train your employees

The first thing you can do to improve efficiency is employee training.

Give them the necessary devices and information they need to complete their tasks faster and more precisely.

You have to go out of your way to support and train your employees to get comfortable with advanced technology to improve productivity.

Automate processes

No business is sustainable without automation and invention.

Therefore, find ways to reduce manual workload so that you not only save time but also increase data accuracy.

You can implement NetSuite integrations to automate different business processes.

Automate financial functions like data entry, bank reconciliation, and financial reporting.

Many businesses make the mistake of hiring a dedicated employee just to handle desk work like cash flow tracking and data entry.

These are tasks that can easily be automated with technology and advanced tools.

So, make sure you apply these cost-reduction techniques for an overall impact.

You can also subscribe to accounting software to speed up your financial processes and improve accuracy.

3. Outsource accounting

Outsourcing has many advantages.

The most obvious one is that you can reduce the cost of a full-time in-house employee.

You will cut down on the cost that would go into employee benefits and other miscellaneous expenses.

By outsourcing certain responsibilities, you can focus on business strategies that you otherwise don’t get the chance to do. So, you wouldn’t stick to the age-old practices, instead, you’ll open up avenues and look into ways to scale your business.

And lastly, you’ll get expertise on board to handle crucial business activities.

They can give you valuable insights to make your business more efficient and profitable.

4. Gain more control over your finances

Is it that easy to gain financial control?

Not really. So what comes under financial control?

Budget Allocation

Budgeting is the most important part of cost control.

A budget is essentially your plan of action to predict and manage your expenses and income for a particular period.

When you create a budget, you know how much you can spend, automatically avoiding overspending.

For large organizations with complex financial structures, using enterprise budgeting tools can further streamline budget allocation, improve forecasting accuracy, and ensure tighter financial control across departments.

Monitoring financial performance

Keep track of your money. You should know where your money is coming from and where it is going.

You must monitor how well your business is doing, and more precisely, which department generates the most income.

Analyze your financial data as it will help you use your money well.

5. Tax compliance

Businesses should reduce costs by avoiding penalties. And the most obvious way to do that is by maintaining compliance standards.

Compliance includes your federal and state taxation along with other registration guidelines.

Now what can you do to ensure compliance? Here are some tips:

- Stay up-to-date with the latest tax development and regulation guidelines.

- Regularly track your finances and maintain accurate reports.

- Follow the guidelines and requirements set by the Securities and Exchange Commission (SEC)

- Pay your taxes on time and prepare them ahead of time to avoid penalties

- Conduct regular financial audits to reduce the chances of errors.

6. Invest in accounting software

Investing in accounting software eliminates human intervention at every step of your financing.

This means you not only get your work done faster, but you also save time and accuracy.

Use accounting software to automate daily tasks like bookkeeping that consume hours from your day.

With automation, you can redirect your energy into strategic initiatives and grow your company.

You should invest in accounting software to improve data accuracy for informed decision-making and get access to real-time financial data for a more nuanced analysis.

Choosing the right accounting software for your business is important.

While QuickBooks Online offers a detailed financial management system with a learning curve, Xero is your go-to option for a cloud software solution.

Whichever software you choose, make sure it aligns with your business goals.

It should help you achieve your objectives whether it is a user-friendly dashboard or scalable features.

7. Promote productivity and stop counting hours

The one reason why you fail to reduce costs is poor leadership.

Your focus should be on improving productivity. And that doesn’t mean you start increasing the working hours.

In fact, if recent studies are to be believed, you should create a flexible culture that strives for employee satisfaction.

The more satisfied you are with your job, the less stressed you’ll be, leading to better workflow and higher productivity.

And the upside to this is reduced cost. You’ll save on office utilities, like electricity and rent.

Adopt work-from-home or hybrid models to promote flexible work culture.

The Bottom Line

There are 7 practical solutions to reducing accounting costs.

Businesses should evaluate their accounting practices and categorize their cost to make cost reductions simpler and more strategic.

The more data-driven your approach is, the better and more effective the results will be.

Ledger Labs, one of the most cost-effective accounting services, has been a key player in the industry, helping businesses with cost reduction by providing complete financial services.

We handle your accounts and support you with your day-to-day bookkeeping.

Book a consultation with us today to understand how you can outsource your financial responsibilities to us.