- CA : 1001 Wilshire Bovd, Los Angeles, CA 90017

- NY: 1178 Broadway, 3rd Floor #3067, New York, NY 10001

Messy books, missed deadlines, and financial blind spots don’t have to be part of running a business.

Ledger Labs handles your accounting end-to-end so you always know where your money is, where it’s going, and what to do next.

Happy Clients

Years in industry

Strong team

We understand your industry’s challenges and are here to provide personalized accounting and bookkeeping services that help you thrive.

Let’s work together to keep your finances on track!

When your books are incorrect, everything else is affected too. You make pricing choices based on numbers you can’t fully trust. You miss tax deductions that no one pointed out. You may face cash flow issues that your reports didn’t warn you about. By the time you notice something is wrong, it might be too late to fix it.

Poor accounting does not just waste your time; it also costs you money, opportunities, and sometimes even your business.

Here’s what most businesses come to us dealing with:

Most business owners don’t need more advice about their finances. They need someone to actually handle them. Here’s exactly what our outsourced accounting and bookkeeping services cover, every month, without you having to ask.

Every transaction is recorded, reconciled, and organized

Filed accurately, on time, every time

Tracked, calculated, and filed across every state

All vendor bills are paid on time

Your invoices are sent and followed up on

Your team is paid right, every cycle

Your numbers and the metrics that actually matter

SKU strategy, inventory levels, and cash flow all aligned.

Most outsourced accounting and bookkeeping services look the same on the surface until something goes wrong. Here’s what actually separates us from every other bookkeeping service provider you’ve worked with or considered.

| Feature | Ledger Labs | Other Accounting & Bookkeeping Firms |

|---|---|---|

| Pricing | Fixed, transparent pricing, no surprises | Higher costs with hidden fees |

| Expertise | Industry-specialized accountants with deep domain experience | Generic bookkeepers with one-size-fits-all processes |

| Financial Strategy | Data-driven strategies built around your growth goals | Basic recordkeeping with no forward-looking insight |

| Scalability | Services that grow as your business grows | Rigid packages that can't adapt |

| Reporting | Real-time dashboards and AI-enabled reporting | Delayed, manual reports delivered too late to act on |

| Cash Flow Management | Proactive monitoring, problems flagged before they hit | Reactive tracking, you find out after the damage is done |

| Tax & Compliance | Full U.S. tax compliance across federal, state, and local | Limited compliance support that leaves gaps |

| Team Structure | Dedicated bookkeeper, accountant, and manager on your account | Whoever is available that month |

| Technology | Cloud-based tools, automation, and software implementation | Outdated systems with manual workarounds |

| Fraud Prevention | Regular audits, reconciliations, and internal controls | No systematic oversight or checks |

Higher costs with hidden fees

Changing your accounting and bookkeeping provider can be stressful. We understand that. You have likely spent a lot of time explaining your business to someone who still didn’t fully understand it. We created our own onboarding process to address this issue.

Here’s what happens from your first call to receiving your first clean report.

We begin by thoroughly assessing your financial records, identifying inefficiencies, and pinpointing areas for cost optimization. This allows us to recognize the areas of improvement and help you put together a robust accounting strategy. We dig into your books to find what’s missing, broken, or holding you back. Then, we lay out exactly what needs fixing — so you’re no longer guessing and finally have a clear path to clean, accurate finances.

As soon as we finalize a comprehensive plan of action for your books, the next step is to deploy this plan. We do this by ensuring we have proper internal and external control of data. Internally, we ensure that financial records are organized, reconciled, and regularly monitored. Externally, we implement secure data-sharing protocols and compliance measures to safeguard financial information.

Accounting is an evolving process, and we continuously refine financial strategies to enhance profitability. We ensure full compliance with tax regulations, conduct regular audits, and provide proactive recommendations to keep your business on the right track. And one of the best ways for us to do this is by building custom apps and workflows for your business - all powered by AI.

Our system provides up-to-date financial reports, allowing you to track performance, monitor key metrics, and make data-driven decisions. With detailed reports and regular insights, you gain complete control over your business finances and witness the financial health of your company improve. Our reporting system helps you identify trends, address potential issues proactively, and optimize cash flow management.

Operations Manager

Allison is a Certified Public Accountant (CPA) and a member of the AICPA. She oversees operations at Ledger Labs, ensuring accurate, compliant financials for hundreds of clients. With experience in both public and private accounting, she builds scalable systems that support fast-growing ecommerce businesses.

Operations Manager

Allison Rinehimer is the Operations Manager at Ledger Labs, where she combines her CPA expertise with a forward-thinking approach to accounting operations and team efficiency. A solutions-oriented problem-solver, she brings a unique ability to align strategic vision with day-to-day execution. With experience across both public and private accounting, Allison leads the development of internal systems that support scalable, high-impact client delivery—powering hundreds of engagements with accuracy and compliance.

Education:

Accountant

Matt brings 7+ years of accounting experience across ecommerce, SaaS, and technology. He specializes in financial reporting, month-end close management, and ERP implementations (including NetSuite transitions). Matt ensures our clients get accurate, timely financials they can rely on for growth decisions.

Accountant

Matt Hidalgo is an Accountant at Ledger Labs, currently on a development path to become a Controller. With over seven years of experience across healthcare advertising, e-commerce, and technology, Matt delivers detail-driven accounting insights that improve financial processes and enhance operational efficiency. He is recognized for his analytical mindset, precision, and ability to strengthen accounting systems in fast-moving environments.

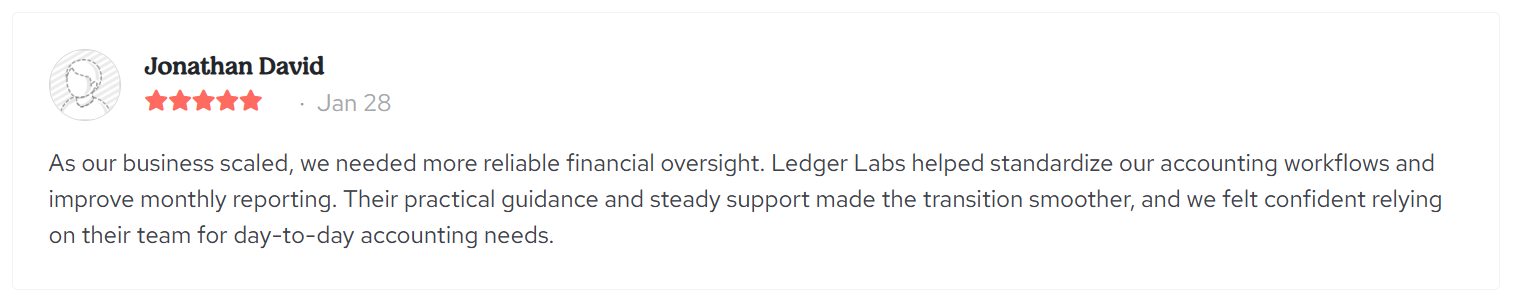

Education:We have a unique business, and almost all the accounting firms we have engaged so far have been unable to get a hold of our business. But Ledger Labs really took the bull by its horn. They understood our business better than us & created a very customized process & systems to streamline our accounting department. We now have detailed step-by-step process documentation, checklists & schedule of reports.

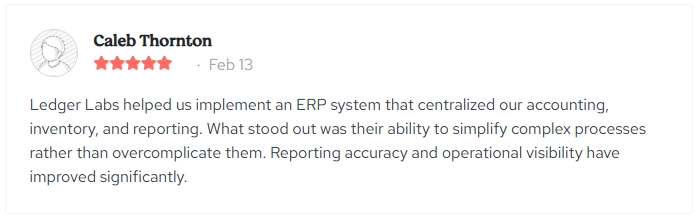

Amanda Fludd CEOLedger Labs found $18K in missed deductions that our old accountant completely missed—same books, same receipts, totally different results. That’s when I knew we were finally working with pros. Since then, they’ve helped us restructure expenses and make tax planning part of the daily flow, not just something we scramble on last minute.

Michael Smith CFOYou will get a dedicated team of 3 members: bookkeeper, accountant and manager who will record and manage your business financials regularly.

Our clients' unflinching trust is what keeps us in business. We've won our hard-earned reputation because:

1. We provide dualified and dedicated accountants

2. We document everything related to your business and its operations.

3. We conduct a thorough and multi-level check before delivering the final reports and financial statements.

Apart from this, word of mouth from our clients has helped us a lot. We also undertake full responsibility for our tasks, actions, and outcomes and do not overcharge you in any way until the assigned task is executed.

We are a good fit if your business is:

1. A US-based organization or a subsidiary

2. In any of the ways, connected with the financial domain or ‘numbers’

3. Reports a yearly revenue of at least 1 million USD, using legal means

Seeking:

1. Advanced and the latest technology

2. Different methods to safeguard all the necessary financial data

3. Different Management strategies and methods to control advanced and high-level accounting needs

4. Advanced, latest, and reliable cost-related and all other types of reporting

5. Methods to smoothen the accounting

6. Methods to develop and increase efficiency using the simplification of accounting

We believe in using various tools and modes to ease up the existing processes of our clients. We execute our deliverables with the help of latest technology. Further, we use all kinds of communication platforms including WhatsApp, MS Teams, Skype, etc. to stay in touch with you. Similarly, our project management tools include Asana and ClickUp.

Your bookkeeping will be executed monthly, quarterly, semi-annually, or annually as you choose. However, the added benefits that you get by updating the books regularly are significant and hence we recommend that all our clients should choose to get their books done monthly.

The closing of books and accounts will be executed by your dedicated accounting and bookkeeping services team on different dates. This will depend upon the type of business, the scale of operations, and other complexities. However, in general, our team closes the previous month’s accounts within the first week of the next month.

In the unlikely event of your choosing to end your contract with us, you can send our team an email regarding the same.

Our team of accounting and bookkeeping experts will begin reviewing your business operations within the first week of your communication. For this, we will require all of your financial statements and data. So we'll prefer that your accountants or bookkeepers can answer our queries. However, it’s not an obligation. We can easily proceed without this assistance as well.

No, if you think your books of accounts are messy and inconclusive, we will clean them up. We will use accurate cloud accounting techniques and platforms to synchronize the data as per your requirements. This will help us both understand them better.

Absolutely! It's your right to ask questions and our priority to answer to them. Your team will always be available during business hours and you can connect with them through phone, message or email.

We will be quite comfortable working with you and for you remotely. Your team of bookkeepers and accountants will be available during business hours and you can connect with them via calls, texts, emails, online meetings, conferences, or any other mode of communication.

No, once you connect with our accounting professionals, you will not need any in-house bookkeeping and accounting staff. Your new team will serve you exclusively and will take care of all your accounting and bookkeeping tasks. However, our team may need to communicate with someone from your office who needn't be an accountant or bookkeeper.

We adopt a brief yet effective onboarding procedure for new clients. We can take care of all your requirements right away. However, it’s better if some time is offered to us for researching your business and its environment. The complete process of understanding your business, optimization of the existing accounting process, policy drafting, execution, and reporting may take somewhat between 30-60 days to complete.

Even if your accountant is away for some reasons, your work from our end will not be hampered in any way. We always work in a team and hence the absence of any account from either side does not affect the regular operations.

Accounting and bookkeeping are delicate matters. One can't rush into the results as it may have negative repercussions. Having said that, after the first ninety days your business will definitely start noticing the ease of accounting and bookkeeping. This duration can also be reduced if the process runs smoothly and we get all the statements and invoices timely from you.

We take your data security seriously. We at Ledger Labs, take all the preventive and safeguarding measures and decisions to ensure that your data is safe at all costs. We spruce the data using multiple encryption levels that can only be accessed by us and the client. Additionally, the two-factor authentication ensures that your data is accessible to only those allowed. We conduct an extensive background check before hiring employees and team(s). Lastly, we also sign a non-disclosure agreement with our clients for increased reliability.

Yes, we at Ledger Labs, will revert your documents as soon as the books are updated or the contract concludes.

Our learnings from years of multidimensional experience have been summarized in these articles!

From saving thousands to scaling fast, these stories highlight how we help businesses grow smarter with real financial strategy and execution.

We use cookies to enhance your experience and analyse traffic. Privacy Policy

Your selection is saved for 1 year.

| Thank you for Signing Up |

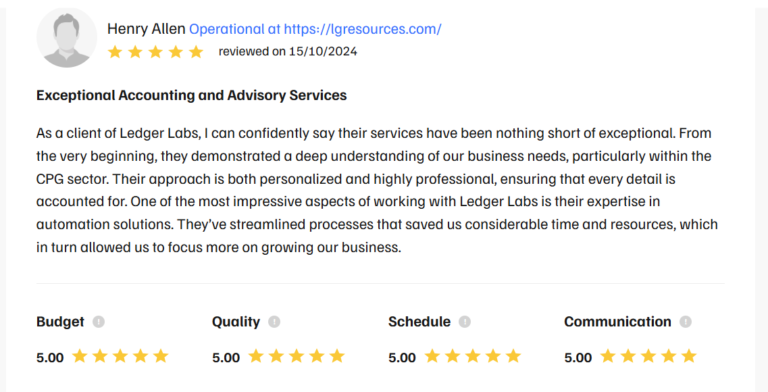

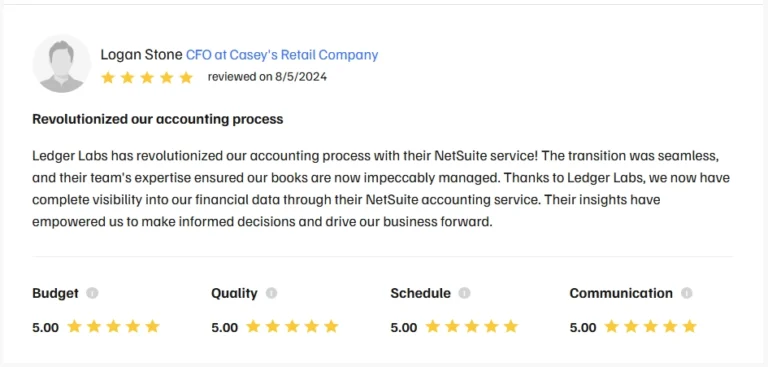

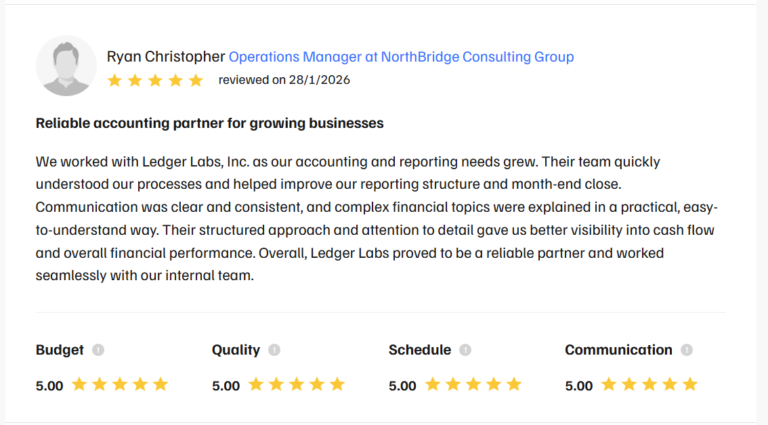

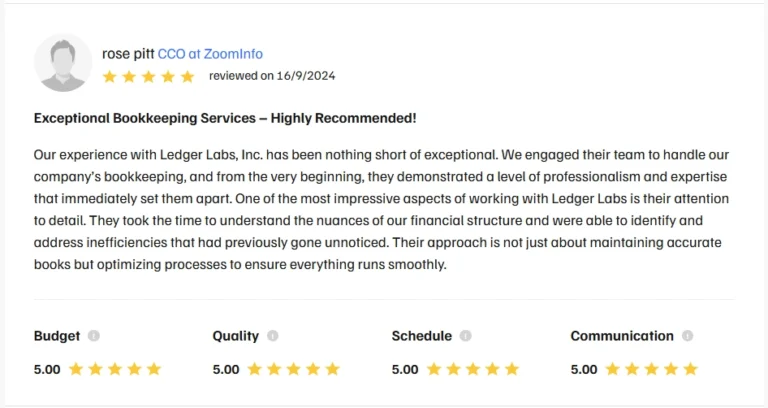

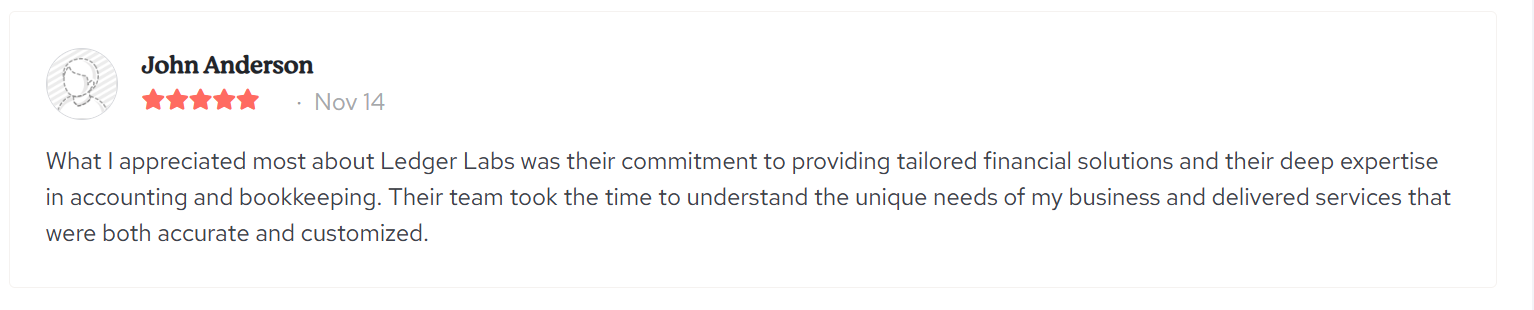

My main problem always has been to know my accurate profits & this is precisely what Ledger Labs helped me with. They went through my entire supply chain costs, my monthly operational expenses, and COGS and got me the correct costing of my goods and the cost of running the business. Now I know how much I need to sell & at what price I should sell it to be profitable.

Ariel Robinson CEO & Founder